JAKARTA (12/08/2025). Kebijakan fiskal untuk kendaraan bermotor di Indonesia berada di persimpangan jalan. Selama lebih dari satu dekade, serangkaian insentif, terutama pembebasan pajak untuk kategori Low Cost Green Car (LCGC), telah diterapkan melalui PP No 41/2013 dengan tujuan mendorong adopsi kendaraan rendah emisi. Namun, alih-alih mempercepat kendaraan hemat energi dengan penerapan Low Carbon Emission Vehicle (LCEV) yang menjadi misi utama dan asbabun nuzul diterbitkannya PP tersebut, kebijakan yang ada justru melahirkan paradoks: beban anggaran negara yang signifikan tanpa dampak proporsional terhadap penurunan emisi gas rumah kaca (GRK).

Pelaksanaan PP No 41/2013 disabotase untuk kepentingan semata mendongkrak penetrasi pasar otomotif nasional yang sedang lesu kala itu akibat penurunan daya beli masyarakat dengan cara pragmatis guna menghadirkan kendaraan yang terjangkau. Selain menghadirkan kendaraan dengan teknologi down sizing yang sangat berbahaya karena turut serta menurunkan safety level demi mencapai target hemat BBM dan harga murah, kebijakan tersebut juga melupakan misi utama penerapan LCEV.

Baru sepuluh tahun kemudian, di tengah kecenderungan global untuk adopsi kendaraan rendah karbon sesuai spirit Perpress No 55/2019 dengan berbagai regulasi terkait yang berusaha merealisasikan amanat UU No 16/2016 tentang Pengesahan Paris Agreement; pemerintah merealisasikan dukungan pada LCEV dengan memberikan insentif fiscal pada Battery Electric Vehicle (BEV). April 2023 Pemerintah mulai memberikan insentif berupa potongan pajak sehingga masayarakat yang membeli BEV hanya membayar 53% pajak dari total 83% pajak yang seharusnya dibayar. Pada praktiknya, pembeli per unit sepeda motor listrik dan mobil listrik masing-masing mendapatkan pengurangan harga Rp 7 juta dan Rp 80 juta. Berlatar bekalang keprihatinan krisis iklim saat itu, berikut prediksi krisis iklim ke depan terutama pada 2100 yang akan semakin parah dengan dampak bencananya, Paris Agreement disepakati sebagai kesepakatan global guna memitigasi GRK demi mencegah krisis iklim yang semakin parah. Adopsi BEV memang menjadi rekomendasi kuat Paris Agreement.

Persoalan belum selesai. ICE technology yang memproduksi kendaraan boros BBM dan mengemisikan karbon tinggi berusaha mempengaruhi kebijakan insentif fiscal bagi BEV di atas. Kebijakan pemerintah terguncang dan mulai mengendurkan insentif fiscal BEV, dengan dalih kesulitas ruang fiscal. Di tengah stagnasi ini, muncul wacana alternatif yang radikal: sebuah skema fiskal berbasis tingkat emisi karbon (feebate/rebate) yang diterapkan pada basis pendapatan netral pada APBN (budget neutrality). Analisis yang disampaikan pada FGD yang diselenggarakan oleh Kementerian Lingkungan Hidup ini (Jakarta, 12/08/2025) mengkaji kegagalan struktural dari kebijakan insentif saat ini dan mengevaluasi potensi sistem cukai karbon dan insentif rendah karbon sebagai solusi yang lebih efektif, adil, dan berkelanjutan untuk pasar otomotif Indonesia.

Efektivitas yang Dipertanyakan

Sejak 2013, instrumen utama pemerintah adalah pembebasan Pajak Penjualan atas Barang Mewah (PPnBM) untuk kendaraan rendah emisi karbon. Namun sebagaimana disinggung di atas implementasinya dinilai sarat dengan distorsi kepentingan industry otomotif semata, sehingga hanya diterapkan pada LCGC.

"Bayangkan, dari tahun 2013 sampai 2023, kurang lebih 10 tahun, yang dapat insentif hanya LCGC," ungkap Ahmad Safrudin, Direktur Eksekutif Komite Penghapusan Bensin Bertimbal (KPBB). Ia menyoroti sifat diskriminatif dari kebijakan tersebut. "Ada kendaraan yang sebenarnya low carbon tetapi ternyata tidak mendapatkan insentif. Contohnya ya LCEV (Low Carbon Emission Vehicle), beberapa varian sudah masuk pada kategori LCEV namun tidak memperoleh insentif karena tidak kategori LCGC.”

Ketergantungan pada APBN juga menjadi kelemahan fatal. Setiap insentif berarti pengurangan pendapatan negara. "Kalau pemerintah terus-terusan memberikan insentif, tentu akan menjadi beban karena penerimaan atau tax revenue pemerintah jauh berkurang," lanjut Safrudin. Ketergantungan ini membuat kebijakan menjadi tidak pasti dan rentan dihentikan (secara poloitik), seperti yang terjadi saat ini yang memicu ketidak-pastian di industri kendaraan listrik.

Biaya Kesehatan Akibat Polusi Udara

Fokus pada insentif tanpa disinsentif bagi kendaraan beremisi tinggi telah mengabaikan biaya eksternalitas yang ditanggung masyarakat. Polusi udara dari sektor transportasi memiliki dampak kesehatan dan ekonomi yang nyata.

"Perlu kita sadari di sini bahwa pencemar udara itu adalah isu lokal dan tanggung jawab kita sendiri," tegas Ibu Dr R Dierjana, seorang akademisi dari ITB. Ia menggarisbawahi potensi krisis pada sistem jaminan kesehatan. "Dampak kesehatan dari pencemaran udara itu membuat ancaman bagi BPJS [jebol]."

Data KPBB memperkuat argumen ini. "Kajian kami tahun 2016, masyarakat Jakarta harus mengeluarkan medical cost, baik pribadi maupun lewat BPJS, itu Rp 51,2 triliun," ungkap Ahmad Safrudin. Biaya ini merepresentasikan beban ekonomi masif yang timbul akibat kebijakan yang gagal mengendalikan sumber polusi secara efektif.

Skema Fiskal Berbasis Karbon (Feebate/Rebate Fiscal Scheme)

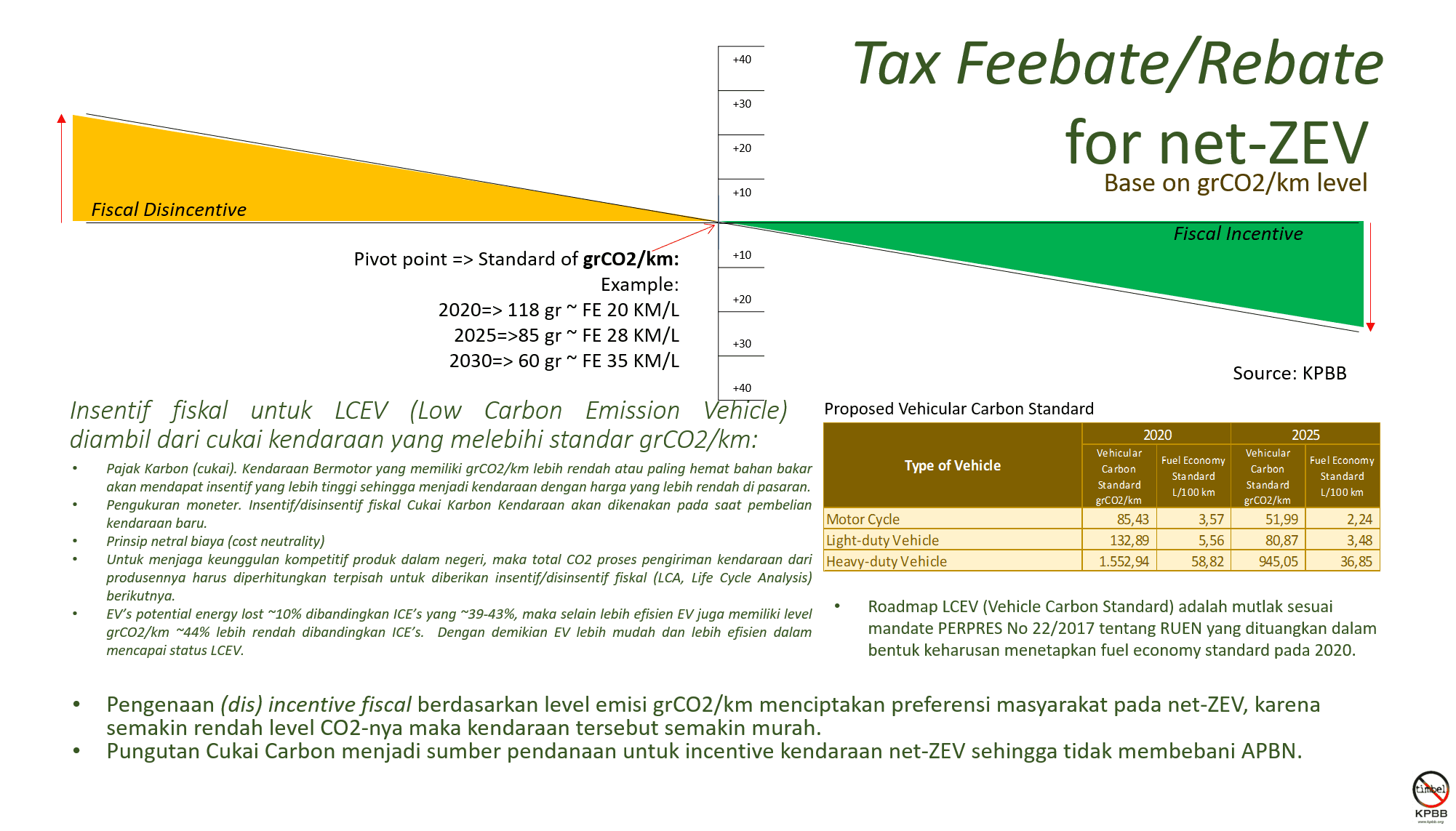

Sebagai solusi atas kelemahan sistemik fiscal bagi kendaraan rendah karbon, KPBB mengusulkan skema feebate/rebate fiscal policy yang terintegrasi dengan tingkat emisi karbon (gr CO2/km).

Mekanisme Kerja dimulai dari Penetapan Standar di mana Pemerintah menetapkan ambang batas emisi karbon untuk setiap kategori kendaraan (grCO2/km). Standard ini bersifat Pivot Point yang ditetapkan sesuai dengan perkembangan teknologi penurunan emisi karbon kendaraan. Berikutnya adalah pengenaan Feebate (Denda) bagi kendaraan apabila emisinya di atas standard berupa cukai karbon secara proporsional dengan tingkat karbonnya. "Semakin tinggi karbonnya ... semakin tinggi pula cukai yang harus dibayarkan. Jadi cukai ini dikenakan atas setiap gram karbon yang melampaui standard dan dikalikan nilai tertentu –harga teknologi penurunan karbon– dan totalnya harus dibayarkan oleh si pembeli kendaraan," jelas Safrudin.

Parallel dengan itu, maka pemerintah juga menyediakan opsi rebate (insentif berupa potongan fiskal). Kendaraan dengan emisi di bawah standar berhak menerima insentif. "Kalau kita membeli kendaraan yang level karbonnya jauh di bawah standar... nanti akan dapat nilai insentif," tambahnya. Nilai insentif ini didasarkan pada kemampuan kendaraan menekan emisi karbon di bawah standard atau ambang batas. Setiap grCO2/km di bawah standard yang ditetapkan akan diperhitungkan sebagai kinerja untuk memperoleh insenti potongan pajak, sehingga kendaraan dengan tingkat karbon rendah akan memiliki harga jual yang lebih murah.

Pada skema ini, pembeli kendaraan punya 2 opsi, tetap membeli kendaraan berkarbon tinggi atau sebaliknya memilih kendaraan berkarbon rendah. Masing-masing punya konsekuensi, kalau mau murah maka akan membeli kendaraan berkarbon rendah, begitu sebaliknya.

Prinsip utamanya adalah netralitas anggaran. Dana yang terkumpul dari denda (feebate) digunakan sepenuhnya untuk mendanai insentif (rebate), sehingga tidak membebani APBN. Dan ketika ada tanda-tanda ruang fiscal pada skema ini mulai deficit, artinya ketika situasi sudah mengarah pada keadaan di mana pemerintah harus menutupi kekurangan penerimaan cukai karbon guna pemberia insentif kendaraan rendah karbon, maka itu adalah saat yang tepat untuk memperketat standard karbon.

Simulasi Pergeseran Harga

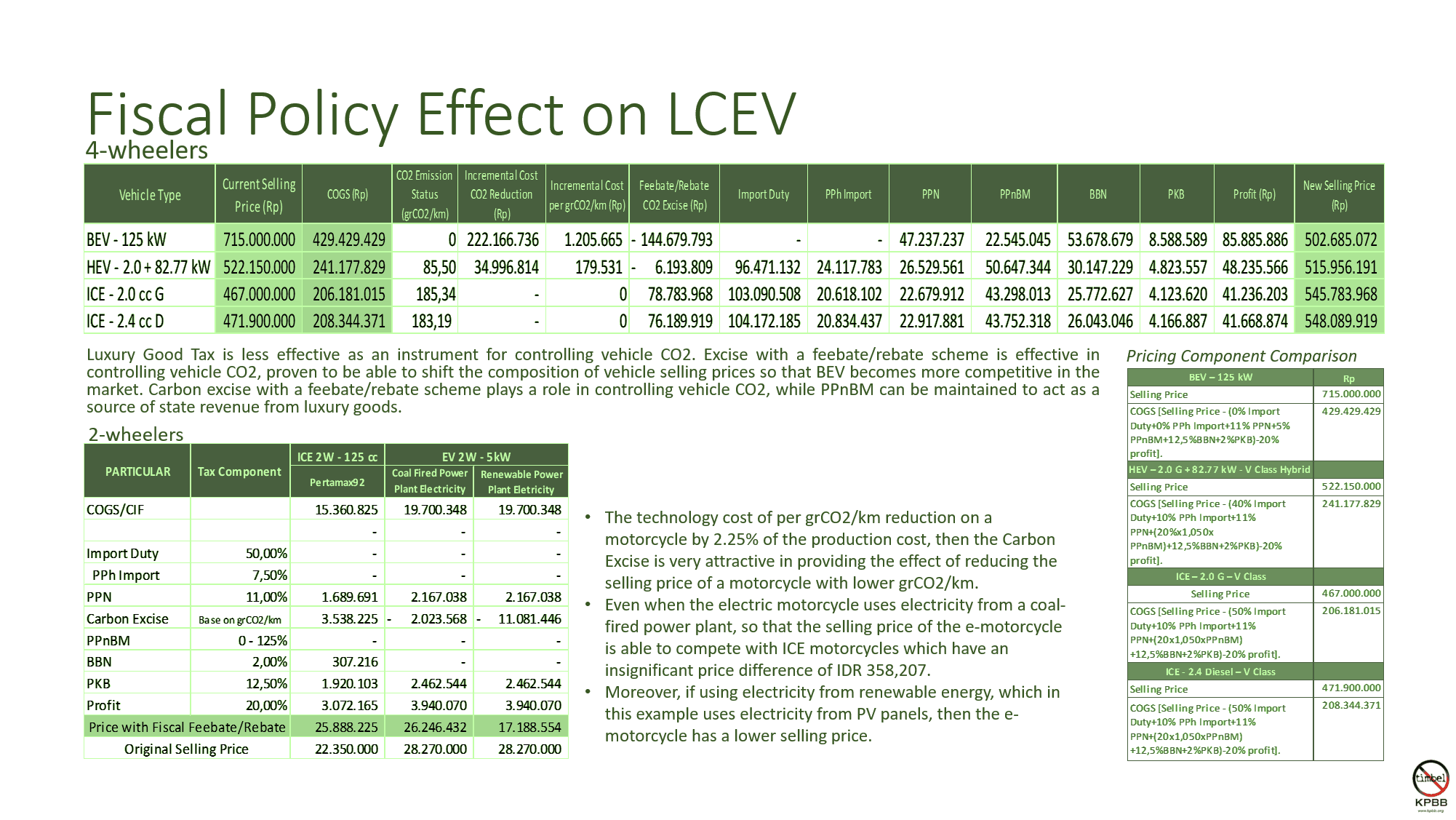

Simulasi KPBB menunjukkan potensi pergeseran harga yang dramatis, yang dapat mengubah perilaku/preferensi konsumen kendaraan secara fundamental. Pada simulasi kendaraan penumpang BEV 125 kW, HEV 2.0+82.77 kW, ICE Bensin 2000 cc dan ICE Diesel 2400 cc; terbukti mampu menggeser pricing position kendaraan. Sebelum skema fiscal ini diterapkan, terbukti bahwa kendaraan BEV memiliki harga yang paling mahal, yaitu Rp 715 juta/unit, kemudian disusul oleh HEV, ICE Diesel dan ICE Bensin masing-masing berharga Rp 522 juta, Rp 471 juta dan Rp 467 juta. Setelah diterapkan feebate/rebate fiscal scheme berbasis tingka karbon kendaraan, maka BEV menjadi kendaraan paling murah, disusul oleh kendaraan HEV, ICE Bensin dan ICE Diesel. Sesuai polluters pay principle, maka kendaraan berkarbon paling tinggi menjadi kendaraan dengan harga paling mahal. Hal ini juga terjadi pada produk sepeda motor. Periksa tabel 2-Wheelers.

Keuntungan dari penerapan feebate/rebate fiscal scheme adalah pemerintah dapat memberikan insentif bagi kendaraan rendah karbon tanpa terbebani berkurangnya ruang fiscal (penurunan pendapatan negara), kebijakan perpajakan kendaraan yang ada (Bea Masuk, PPh Impor, PPN, BBN, PKB) tetap diberlakukan sebagai peluang penerinaan negara, tidak terjadi diskriminasi atas penggunaan teknologi, potensi berjalannya program competitive advantage produksi kendaraan rendah karbon dalam negeri, kendaraan rendah karbon seperti kendaraan listrik menjadi lebih kompetitif secara harga, menciptakan mekanisme pasar yang mendorong adopsi teknologi bersih, bergesernya preferensi pasar pada kendaraan rendah karbon sehingga sangat efektif mencapai ENDC 2030 maupun NZE 2045 dari sector otomotif.

Penutup

Indonesia kini berada di sebuah persimpangan krusial. Analisis menunjukkan bahwa pendekatan insentif fiskal konvensional selama satu dekade terakhir tidak hanya gagal mengakselerasi transisi energi, tetapi juga membebani keuangan negara dan mendistorsi pasar. Di sisi lain, sebuah alternatif berbasis mekanisme pasar melalui skema feebate/rebate fiscal policy menawarkan solusi yang secara konseptual lebih adil, efektif, dan berkelanjutan karena tidak bergantung pada APBN.

Namun, jalan menuju implementasi dihadapkan pada dua tantangan laten. Pertama, potensi resistensi dari pelaku industri yang masih bertahan dengan teknologi beremisi tinggi. Kedua, dan yang paling krusial, adalah fragmentasi kebijakan antar-kementerian yang hingga kini berjalan tanpa sinkronisasi yang padu. Seperti yang disoroti oleh perwakilan industri, saat ini "tidak ada yang menjadi dirijen orkestra ini".

Pada akhirnya, transformasi ini bukanlah persoalan teknis semata, melainkan sebuah ujian kemauan politik. Peta jalan yang jelas, dimulai dari pembentukan payung hukum hingga proyek percontohan, adalah langkah yang niscaya. Keberhasilan untuk beralih dari model subsidi yang tidak efektif menuju mekanisme berbasis pasar akan menentukan apakah Indonesia mampu mendobrak stagnasi, mencapai target Net Zero Emission 2045, sekaligus mengurangi beban biaya kesehatan publik yang mencapai puluhan triliun rupiah.

Sebagaimana ditekankan dalam FGD di atas, momentumnya adalah sekarang, "Standard Karbon Kendaraan Bermotor harus segera ditetapkan. Standard karbon sebagai acuan pengendalian tingkat karbon kendaraan bermotor melalui instrument insentif/disinsentif fiskal." Pertanyaannya bukan lagi 'apakah' perubahan ini perlu, tetapi 'seberapa cepat' para pembuat kebijakan mampu mengorkestrasi langkah-langkah transformatif menuju NZE 2045 ini. oo0oo (SK/AS).